LAVCA Members can log in and download an accompanying LAVCA Data Pack for 2022 fundraising and disclosed closings; exit totals and highlighted exits; all disclosed transactions, sortable by stage, sector and HQ; stage analysis for the major markets; and sector breakouts with year-over-year growth.

IN THIS REPORT

- VC INVESTMENT IN LATIN AMERICA

- VENTURE DEBT & CREDIT: OPPORTUNITIES FOR STRUCTURED FINANCING

- STARTUP FUNDRAISING IN A MARKET CORRECTION

- ROUND SIZE ANALYSIS

- 2022 DISCLOSED VC INVESTMENTS OVER USD100M

- MAPPING THE MAJOR MARKETS

- TOP SECTORS

- EMERGING SECTOR TRENDS: A GLOBAL MARKETS POV

- MOST ACTIVE INVESTORS

- METHODOLOGY

VC INVESTMENT IN LATIN AMERICA

Despite a significant downturn in VC investment compared to 2021, VC investors deployed USD7.8b across a record 1,114 deals in 2022.

VC remained the second largest asset class in Latin America as a proportion of total private capital invested, capturing 28% of total dollars and 82% of all private capital transactions in 2022. VC deployment was highly concentrated in the first months of the year, with 72% of VC dollars invested in 1H 2022.

Seed funding proved to be the most resilient investment stage with investment surpassing USD1b in 2022, up from ~USD650m in 2021 and ~USD300m in 2020, driven by multi-stage funds’ increased exposure to early entrepreneurs coupled with a growing number of emerging fund managers.

Late-stage financings were the most affected by the investment pullback, with a 79% decline in capital deployed across Series C+ rounds compared to 2021. Startups increasingly opted to raise non-dilutive capital, with venture debt seeing positive growth and reaching a record USD1.2b across 47 transactions.

VENTURE DEBT & CREDIT: OPPORTUNITIES FOR STRUCTURED FINANCING

LAVCA tracked a record year in venture debt financing in 2022, with USD1.2b deployed across 47 transactions, following the all-time record in 2021 of USD833m across 22 deals.

Fintech and proptech concentrated the largest debt tranches, with founders actively securing structured financing from global and local investors including Partners for Growth, Hayfin Capital Management, Victory Park Capital, TriplePoint Capital, Architect Capital, Addem Capital and Anteris Capital.

Given the late-stage contraction, startups also turned to local and international banks and secured at least USD1.5b in credit lines to support their lending origination practices.*

*Data not included in LAVCA aggregate statistics.

STARTUP FUNDRAISING IN A MARKET CORRECTION

Founders are adjusting fundraising expectations to current market conditions. Notably, seed founders are taking longer to fundraise, while most late-stage startups are extending runway and avoiding going to the market, according to LAVCA’s 2023 Startup Founders Survey of 160+ VC-backed founders who raised at least one round of financing during 2021 – 1H 2022.

A significant share of founders have also opted for critical operating changes to their original company roadmap in order to prioritize sustained growth through a healthy balance sheet and sound unit economics. The most common operating changes include reductions in workforce, freezes in new hires, as well as limiting marketing and sales expenses. View LAVCA’s full 2023 Startup Founders Survey.

ROUND SIZE ANALYSIS

The average ticket size for early and late-stage deals declined after record highs in 2021, indicating smaller checks for Series A and above in 2022. On average, seed tickets remained above historic levels and reached new heights in 2022.

The median VC round size was still three times higher for early and late-stage deals in 2022 compared to 2020, driven by big tickets over USD100m raised primarily during the first half of 2022.

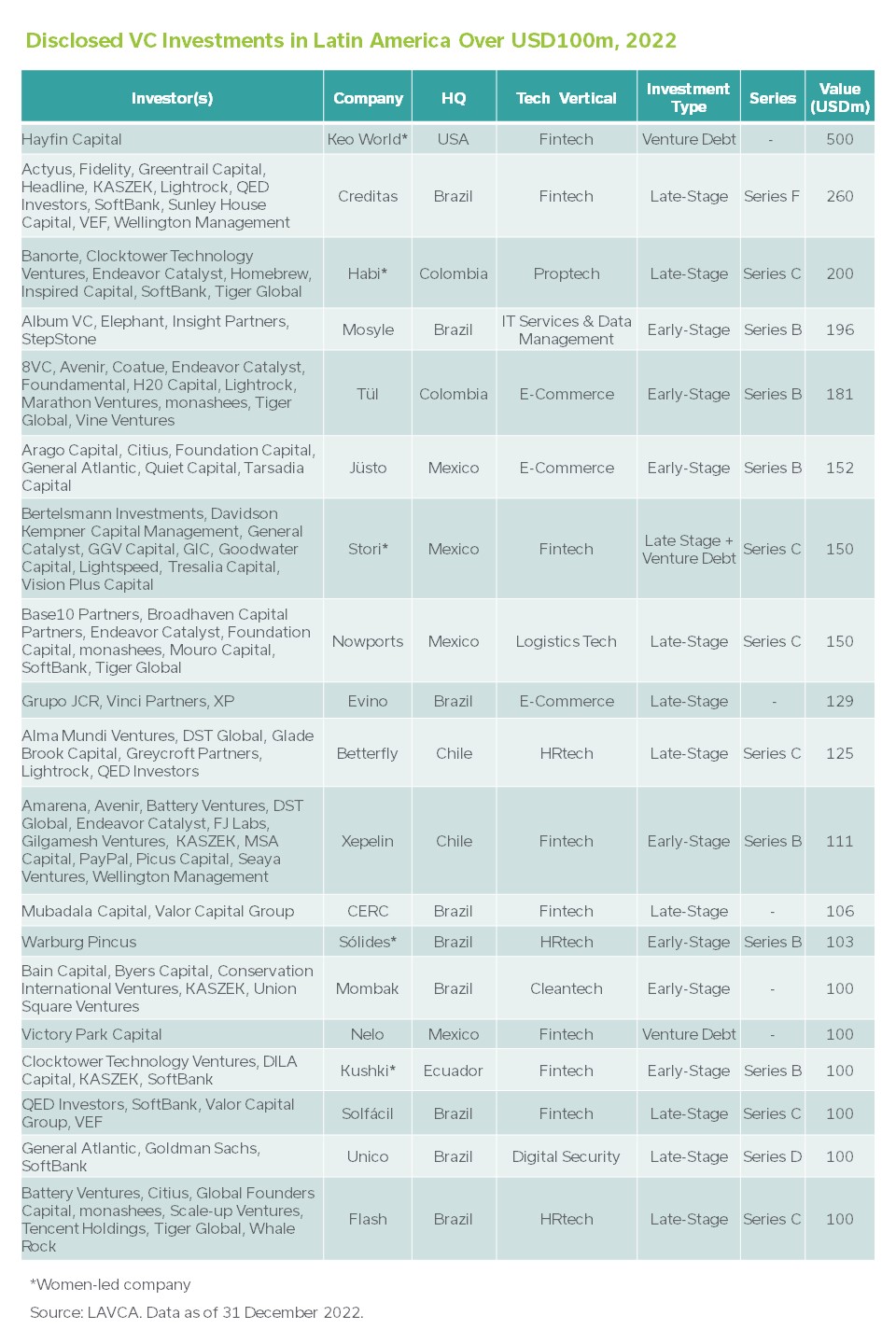

2022 DISCLOSED VC INVESTMENTS OVER USD100M

Latin American startups raised 19 rounds above USD100m, with 15 of them closing during the first half of 2022, as Latin American entrepreneurs leveraged the financing momentum from 2021. Notably, six of these rounds were raised by companies with a disclosed valuation of USD1b+: Betterfly, Creditas, Habi, Kushki, Nowports, Stori and Unico.

Miami-based BNPL platform Keo World’s USD500m round led by Hayfin Capital was the largest disclosed round in 2022 and the largest venture debt financing on record.

Fintech remained the dominant sector of investment, with eight transactions over USD100m raised by companies in the space. HRtech is represented for the first time on this list with Brazilians Sólides’ ~USD103m Series B, Flash’s USD100m Series C and Chilean Betterfly’s ~USD125m Series C.

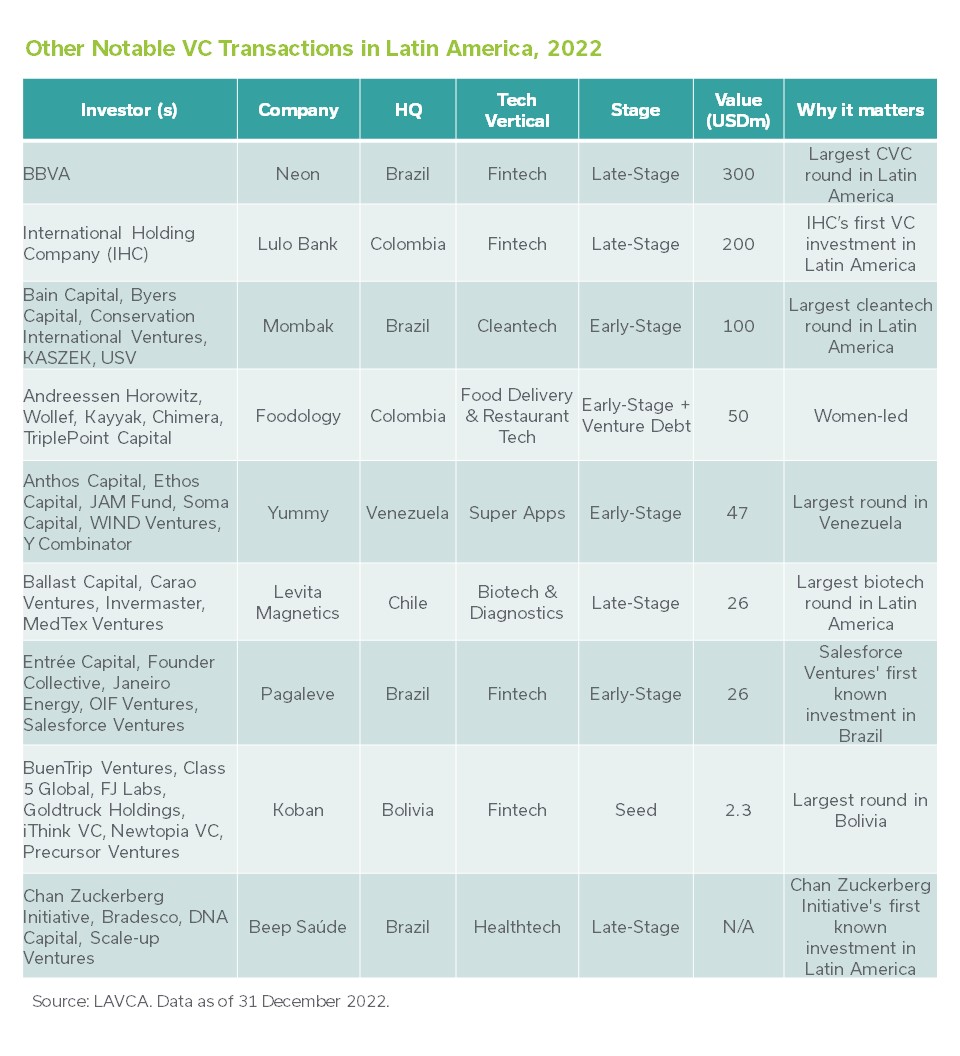

OTHER NOTABLE TRANSACTIONS

MAPPING THE MAJOR MARKETS

Brazil, Mexico and Colombia captured 77% of all VC investment in 2022, on par with the 81% of all dollars invested in 2021. Major markets saw significant investment adjustments ranging from a 24% decline in Colombia to a 72% contraction in Argentina, as no late-stage transactions were recorded in the country for 2022. Even with the slowdown in activity, all major markets still attracted significantly more capital than in 2020.

Peru saw a 63% decline in total investment primarily explained by a reduction in early stage investment from USD103m in 2021 to USD7m in 2022. In 2021, Crehana’s raised a USD70m round – the largest in the history of the country – and e-commerce Favo’s raised rounds amounting to USD30m+.

While Ecuador stands as the only major market with positive growth for total venture investment, 89% of the capital invested is attributed to fintech Kushki’s USD100m Series B, the largest round of its kind for an Ecuadorian startup, surpassing Kushki’s own record set in 2021 with a USD86m round.

Despite the pullback, Latin America reached all-time seed stage records across all major markets. Investor interest in seed stage opportunities also drove double-digit growth in deal count across all markets except Brazil. Colombia saw the fastest growth in seed investment, more than doubling from USD69m in 2021 to USD141m in 2022.

Chile saw the largest Series B in its history, with Xepelin’s USD111m round led by KASZEK and Avenir Growth.

TOP SECTORS

Fintech remained the leading sector for capital invested, capturing 43% of all dollars in 2022, up from 39% in 2021.

Capital remained heavily concentrated in a handful of sectors, with 74% of all VC investment in 2022 attributed to fintech, e-commerce, HRtech, proptech and logistics – a modest contraction from their 80% share in 2021.

Edtech saw one of the largest reductions in financing, with USD84m invested in 2022, down from USD427m in 2021. Notably, the five largest rounds in the sector totaled USD52m in 2022, while the same number of deals in 2021 amounted to USD291m.

BRAZIL | HRtech climbed to the second largest sector in Brazil in 2022, taking e-commerce’s place with USD343m across 29 deals. Notable HRtech rounds included Sólides (~USD103m), Guppy (~USD93m) and Flash (USD100m), which captured 86% of investment in the vertical in the country.

MEXICO | Logistics and e-commerce represented 37% of all investment in Mexico, a 20% contraction compared to their 47% share in 2021, while fintech increased its dominance to 51% of all capital deployed.

COLOMBIA | Proptech led investment in Colombia for the first time, with USD325m invested across 10 rounds. Notable rounds include Habi (USD275m over two rounds) and Castia (USD33m).

EMERGING SECTOR TRENDS: A GLOBAL MARKETS POV

Cleantech: From Reforestation to Renewable Energy

Cleantech climbed up to the seventh most funded sector in the region, surpassing verticals that had historically attracted more investment such as healthtech and food delivery. Notable cleantech investments from 2022 include Mombak (USD100m), EuReciclo (~USD20.3m), Sistema.bio (~USD15.6m) and Lemon Energia (~USD11.7m).

Latin American cleantech is beginning to capture larger rounds of investment under similar themes that have raised substantial capital in other global markets in recent years, including China and more recently India. View GPCA’s 2023 Global Trends in Tech for insights on VC investment in Africa, India, China, Southeast Asia, Central and Eastern Europe and the Middle East.

Biotech: From Robot Assisted Surgeries to Gene Editing

Biotech saw a 3.2x increase in investment in 2022 compared to 2021 with seed and early stage rounds for Levita Magnetics (USD26m), Stamm Biotech (USD17m) and Autem Medical (USD10m).

Total investment in biotech amounted to USD69m, with notable participation of both healthtech funds with an adjacent focus on the sector — such as Yaya Capital, CITES and Hospital Albert Einstein’s CVC fund managed by Vox Capital —and an emerging cohort of biotech-specific funds such as Ganesha Lab and Vesper Ventures.

MOST ACTIVE INVESTORS

LAVCA Members can download our accompanying LAVCA Data Pack for 2022 fundraising and disclosed closings; exit totals and highlighted exits; all disclosed transactions, sortable by stage, sector and HQ; stage analysis for the major markets; and sector breakouts with year-over-year sector growth.

METHODOLOGY

LAVCA Industry Data & Analysis provides insight into the fundraising, investment and exit activity among private equity funds investing in the Latin American region. Since 2008, LAVCA has conducted the Fund Manager Survey on PE/VC activity in Latin America. Year-on-year trend data is modeled from LAVCA surveys. Click here for the complete LAVCA Industry Data methodology.

ADDITIONAL READING

LAVCA 2023 Industry Data and Analysis